Section 4 Income Tax Act Malaysia

Chapter 1

Chapter 5 Non Business Income Students

Taxation Principles Dividend Interest Rental Royalty And Other So

Chapter 5 Non Business Income Students

Taxation Principles Dividend Interest Rental Royalty And Other So

Chapter 5 Non Business Income Students

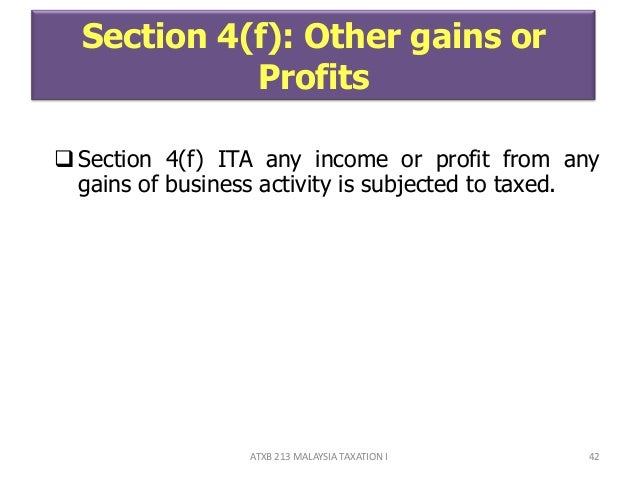

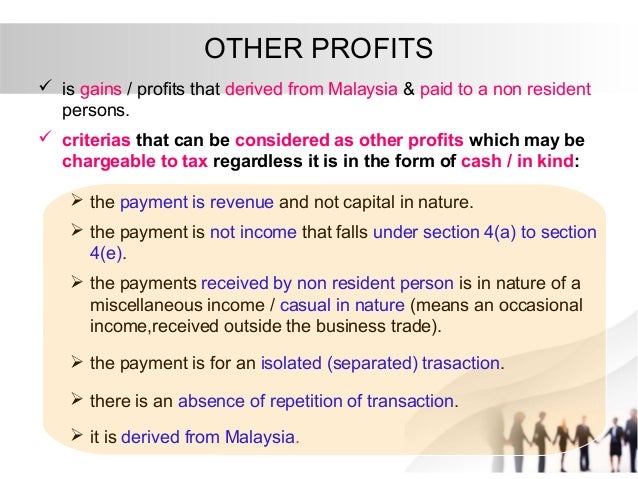

Section 4 f of the income tax act 1967 the act which is derived from malaysia and received by a nonresident is subject to wt of 10 under section 109f of the act.

Section 4 income tax act malaysia. Laws of malaysia act 53 income tax act 1967 arrangement of sections part i preliminary section 1. Income under section 4 f ita 1967. This is due to the inadequacies of section 4 income tax act 1967 in effectively defining income. Charge of income tax 3 a.

I the calculation of a will be based only on the income subject to paragraph 4 a of the act in respect of the gains or profits from a business. Laws of malaysia act 53 arrangement of sections income tax act 1967 part i preliminary section 1. It sets out the interpretation of the director general of inland revenue in respect of the particular tax law and the policy and procedure that. The determination of whether a payment made to a non resident falls under section 4 f depends on the facts and circumstances of each case.

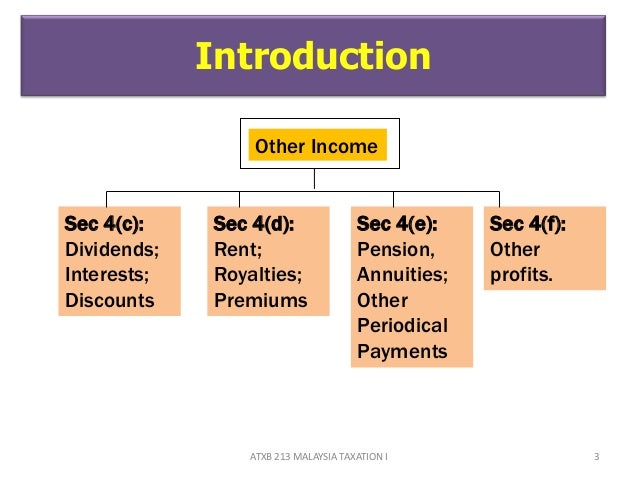

Non chargeability to tax in respect of offshore business activity 3c deleted 4. Income falling under section 4 f of the income tax act 1967 ita 1967 includes any other income that is not obtained from business employment dividends interests discounts rents royalties premiums pensions or annuities. Generally you are only taxed for the profit that you or your business earns. Interpretation part ii imposition and general characteristics of the tax 3.

Short title and commencement 2. Non chargeability to tax in respect of offshore business activity 3 c. Payments that are made to nr payee in respect of the above income are subject. A public ruling as provided for under section 138a of the income tax act 1967 is issued for the purpose of providing guidance for the public and officers of the inland revenue board malaysia.

Perusing the cases involving income tax it is obvious that most of the cases revolve around issue of what constitutes income. Ii the calculation of a is based on how the taxpayer ascertained their business adjusted income or loss under the act without applying section 140c of the act. Charge of income tax 3a deleted 3b. Charge of income tax 3 a.

Interpretation part ii imposition and general characteristics of the tax 3. Short title and commencement 2. Short title and commencement 2. Section 33 1 of the income tax act 1967 ita reads as follows.

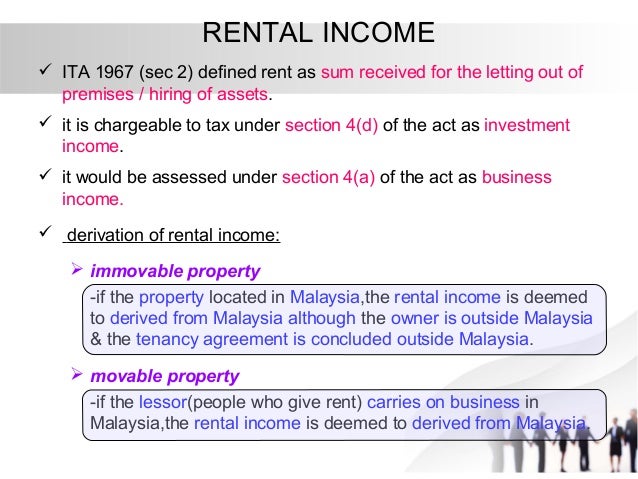

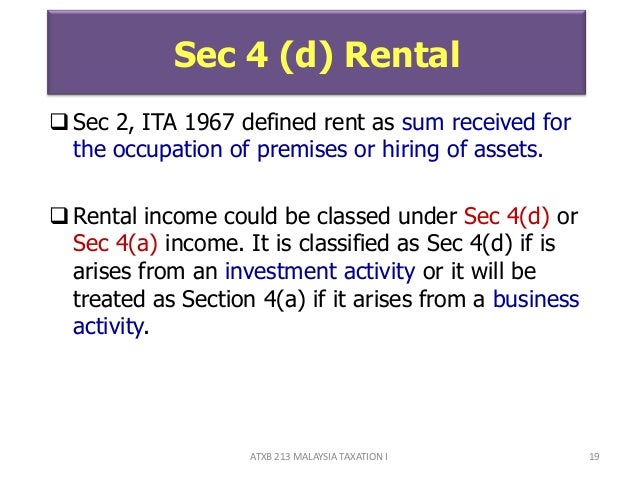

When rental income is assessed under section 4 d it has to be grouped into three sources namely residential properties commercial properties and vacant land. Section 4 a or section d income. As a guidance the criteria. Non chargeability to tax in respect of offshore business activity 3 c.

Rental income is generally assessed under section 4 d rental income of the income tax act and is seen as income from investment. Revolves around section 4 income tax act 1967 which defines income. Malaysia s tax season is back with businesses preparing to file their income tax returns. As such there s no better time for a refresher course on how to lower your chargeable income.

Chapter 5 Non Business Income Students

Chapter 5 Non Business Income Students

Chapter 5 Non Business Income Students

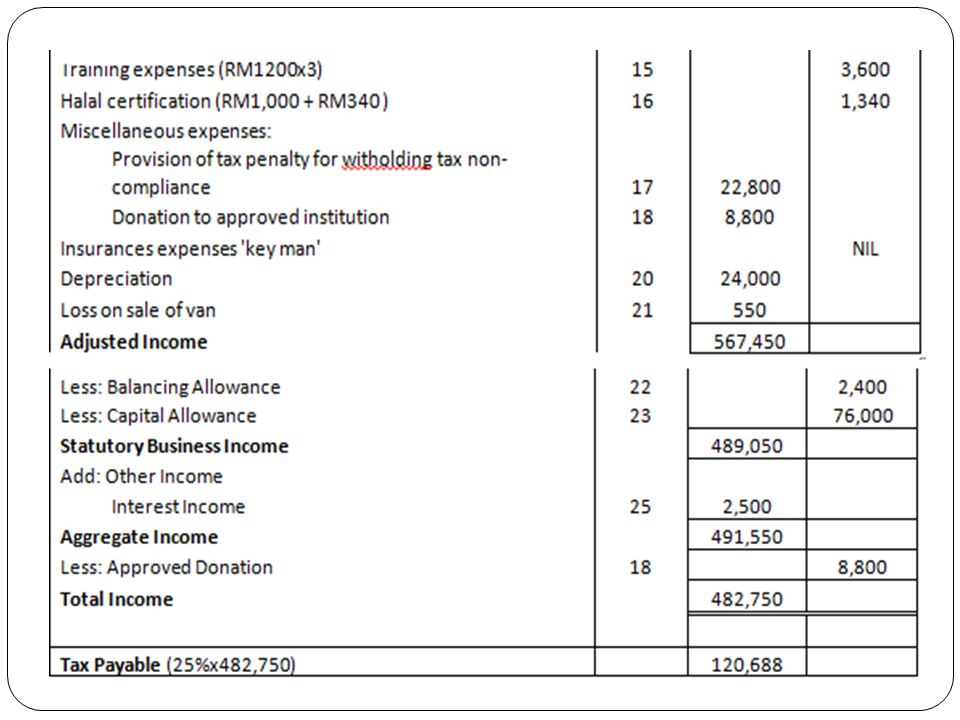

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Chapter 6 Business Income Students 1

Chapter 4 B Employment Income

Ppt Tutorial 1 Introduction To Income Tax Law Powerpoint Presentation Id 3473088

Chapter 5 Non Business Income Students

Tax Planning On Rental Income Afc Chartered Accountants Audit Tax Advisory And Accounting

Taxation Principles Dividend Interest Rental Royalty And Other So

Chapter 4 A Employment Income Stds 1

Section 4 F Income Tax Act 1967