Benefit In Kind Malaysia 2019

Https Mfpc Org My Wp Content Uploads 2019 02 Mfpc Cpd Programme On 3 March 2019 Slide Handout Pdf

Public Ruling 11 2019 Benefits In Kind St Partners Plt Chartered Accountants Malaysia Facebook

Chapter 4 B Employment Income

Benefits In Kind Bik

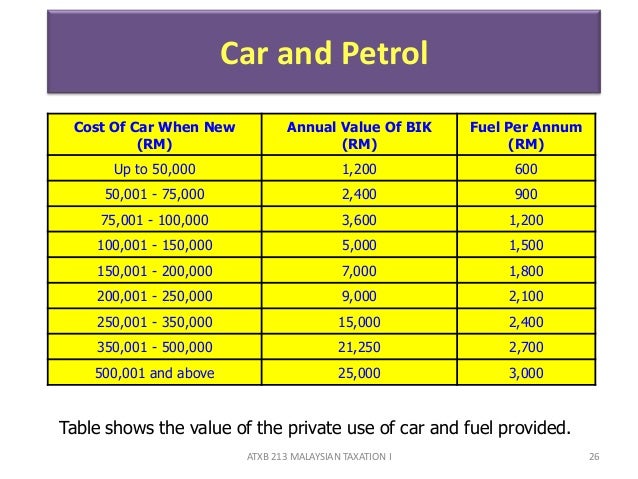

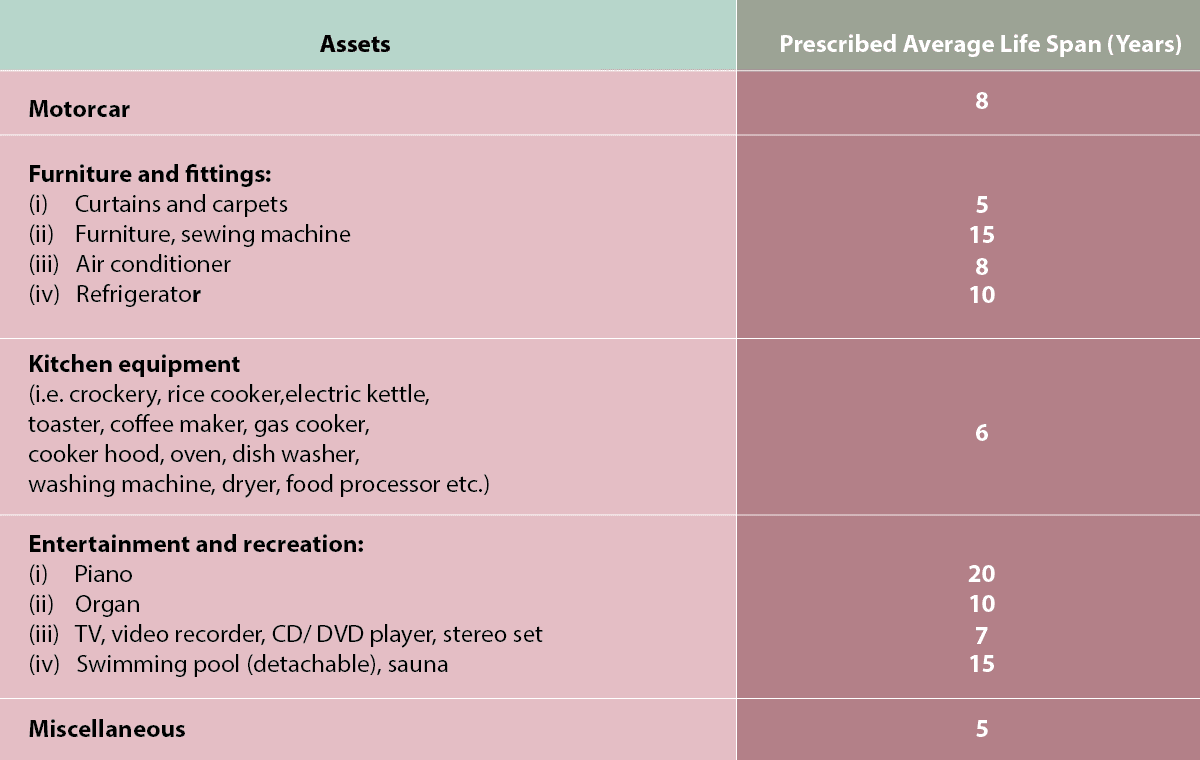

Benefit In Kind Motor Vehicles Malaysia 2019 Table

Malaysia Personal Income Tax Guide 2018 Ya 2017

Inland revenue board of malaysia benefits in kind public ruling no.

Benefit in kind malaysia 2019. 2018 2019 malaysian tax booklet 7 scope of taxation income tax in malaysia is imposed on income accruing in or derived from malaysia except for income of a resident company carrying on a business of air sea transport banking or insurance which is assessable on a world income scope. A further clarification on benefits in kind in the form of goods and services offered at discounted prices. Accommodation or motorcars provided by employers to their employees are treated as income of the employees. Types of benefits comments.

Generally non cash benefits e g. Income attributable to a labuan business. 2 2004 issued on 8 november 2004. 15 march 2013 pages 3 of 31 b any appointment or office whether public or not and whether or not that relationship subsists for which the remuneration is payable.

11 2019 date of publication. Motorcar and petrol driver gardener etc. 12 december 2019 page 1 of 27 1. Certain benefits in kind pertaining to consumable services are not eligible for taxation.

Application to talent corporation malaysia berhad from 1 january 2018 to 31 december 2019. And one should also be awar. 5 2019 inland revenue board of malaysia date of publication. Perquisites are taxable under paragraph.

Perquisites means benefits that are convertible into money received by an. Objective the objective of this public ruling pr is to explain a the tax treatment in relation to benefit in kind bik received by an employee from his employer for exercising an employment and. 19 november 2019 4 2 perquisites are benefits in cash or in kind which are convertible into money received by an employee from his employer or from third parties in respect of having or exercising an employment. Benefits that foster goodwill or promote camaraderie among staff.

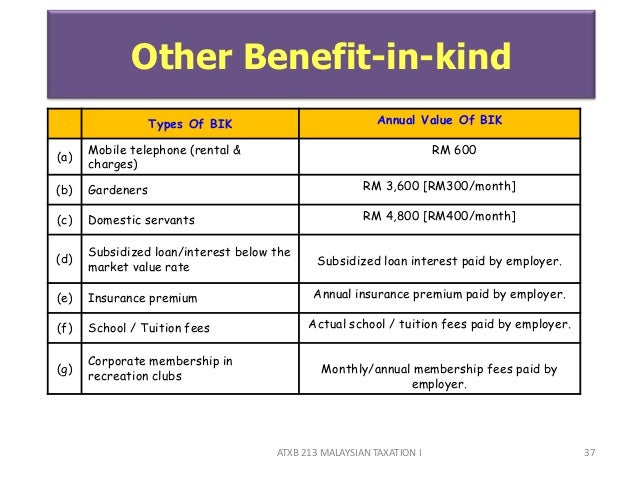

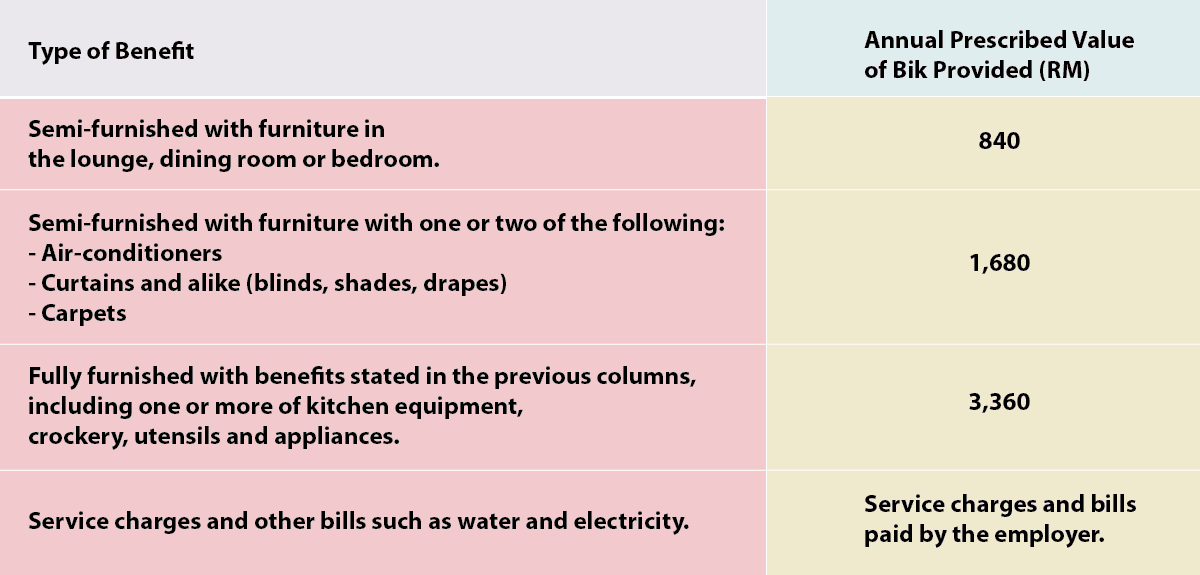

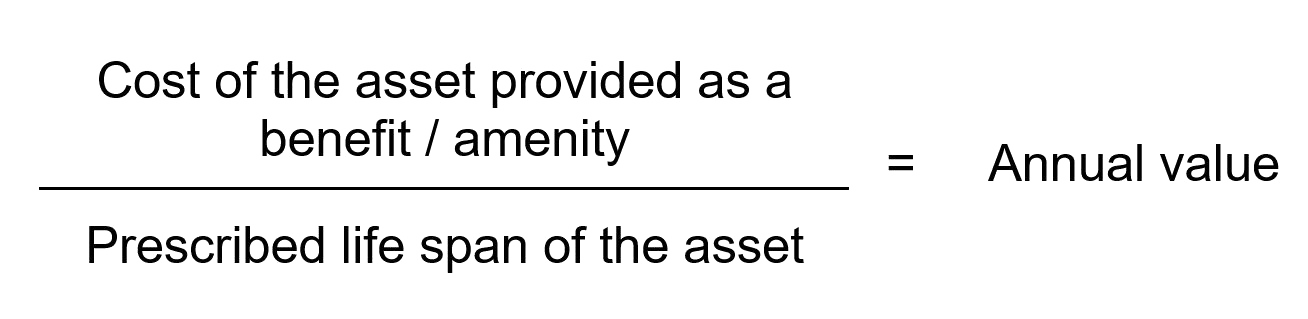

These benefits are called benefits in kind bik. 19 benefits in kind exemptions. Examples of consumable services are dental care childcare benefits food drinks specially arranged transportation between pick up points and special discounts for consumable products that cannot be resold such as food or toiletries etc. Each benefit in kind must be prescribed a monetary value in order to be taxed and this can be done through the formula method or the prescribed method.

2 2 however there are certain benefits in kind which are either exempted from tax or are regarded as not taxable. These benefits in kind are mentioned in paragraphs 4 3 and 4 4 of the public ruling no. There are several tax rules governing how these benefits are valued and reported for tax purposes. There are a few tax exemptions for benefits in kind but benefits like cars furniture and personal drivers are subjected to income tax.

3 2013 date of issue.

Benefit In Kind Motor Vehicles Malaysia 2019 Table

Employment Income

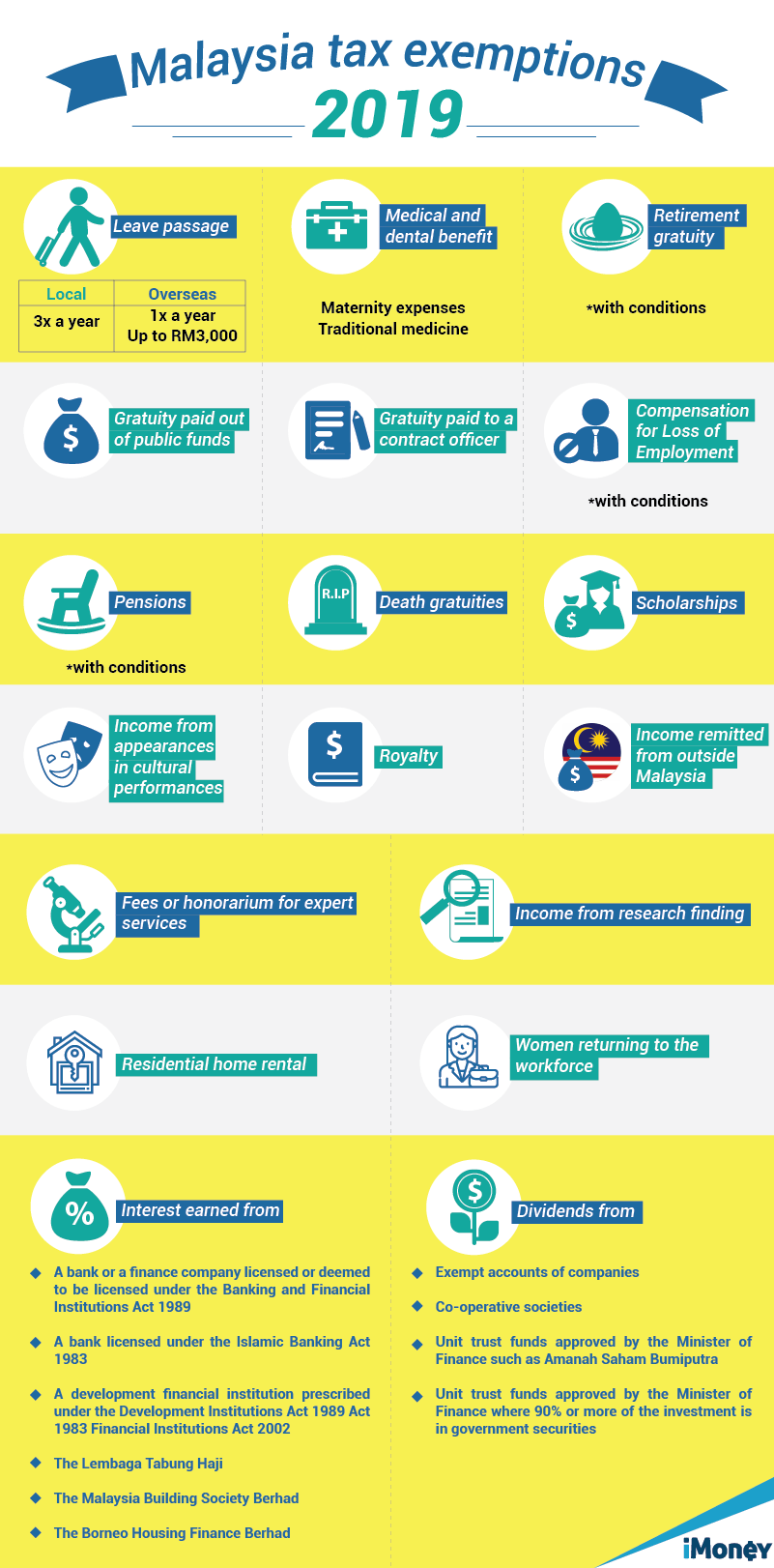

Get More Tax Exemptions For Income Tax In Malaysia Imoney

Malaysia Personal Income Tax Guide 2018 Ya 2017

Public Ruling Benefit In Kind Pac150 Intec Studocu

Smeinfo Understanding Tax

Individual Income Tax In Malaysia For Expatriates

Benefits In Kind Bik

Real Property Gains Tax Rpgt In Malaysia 2020

Smeinfo Understanding Tax

Malaysian Tax Issues For Expats Activpayroll

Malaysia Income Tax An A Z Glossary

Smeinfo Understanding Tax